CA's Housing Policy flawed ?

Evidence from Residential Vacancy Chains 2024 paper by

Valentine Gilbert

VIDEO: MYTH of the "Vacancy Chain" effect on Affordable Housing:

https://youtu.be/tD9kngxSrmM

CA not

focused on VERY LOW income families

https://www.youtube.com/watch?v=BekIUiZQPmE

CA's flawed

"Vacancy Chain" effect on

Affordable Housing

| |

|

REBUTTAL |

The California Policy to promote housing, ( not

just for LOW income households, but for MODERATE and ABOVE MODERATE income Households),

is based on a

2019 working paper by economist

Evan Mast

titled

"The Effect of New Market-Rate Housing on the Regional Housing Market".

( The VACANCY CHAIN from a household's move to a new Market Rate home.

)

This paper is frequently cited to justify policies that promote the

construction of "MODERATE and ABOVE MODERATE" (market-rate or luxury)

housing as a primary tool for broader Affordability.

But Mast's paper tracks

people moving, not

actual rent prices.

And there's a more recent STUDY that contradicts the paper : a 2024 paper by

Valentine Gilbert, VACANCY CHAINS are

often shorter than previously estimated and that new suburban housing has almost no measurable

effect on low-income urban

affordability.

| Most vacancies are created within one year of

the initial move. |

| New suburban single-family housing has a negligible

effect on urban housing affordability.

Each new suburban home leads to only 0.015 moves in low-income,

high-density urban neighborhoods. |

| High-income urban multifamily housing primarily

creates vacancies in other high-income tracts (71% in the first round). |

Summary

Research into how different housing submarkets are interconnected through

residential vacancy chains—the series of moves initiated by the

construction of a new housing unit. By analyzing administrative data on the

residential histories of the U.S. population and conducting economic

simulations, the research evaluates whether suburban housing expansion can

alleviate the housing affordability crisis in dense urban centers.

Critical Takeaways:

| Vacancy Chains are Short: Approximately 90% of vacancy chains

initiated by new construction end within three migration rounds.

Most vacancies are created within one year of the

initial move. |

| Limited Cross-Market Impact: New suburban

single-family housing has a negligible effect on urban housing

affordability. Each new suburban home leads to only 0.015 moves in

low-income, high-density urban neighborhoods. |

| Submarket Stickiness: While vacancy chains do connect disparate

submarkets (e.g., high-income to low-income), the connections are weak.

High-income urban multifamily housing primarily

creates vacancies in other high-income tracts (71% in the first round). |

| Predictive Power of Vacancies: The number of vacancies created in

a neighborhood is as strong a predictor of price effects as complex,

model-derived substitution effects, making vacancy chains a practical metric

for predicting the non-local impacts of new housing. |

| The Scale Paradox: Although suburban housing is less efficient at

creating urban vacancies on a per-unit basis than urban multifamily housing,

the sheer volume of suburban construction (accounting for 80% of supply

growth) means it has collectively created more total vacancies in low-income

urban tracts than new high-income urban developments. |

1. The Context: Urban Demand vs. Suburban Supply

Over the past thirty years, U.S. cities have experienced a divergence in

housing trends. Real home prices and rents in dense urban centers have grown

more rapidly than in suburban areas (45% vs. 30% between 1990 and 2018).

Conversely, 80% of new housing supply growth occurred in low-density suburbs,

while the 10% of tracts closest to city centers accounted for less than 3% of

supply growth.

This raises a fundamental policy question: Can suburban expansion reduce

urban costs, or must cities grow denser to become affordable? The research

addresses this by examining the degree of residential mobility between these

submarkets.

2. Understanding Residential Vacancy Chains

A vacancy chain is the sequence of residential moves triggered by a single

new unit:

- First Link: A household moves into a newly constructed unit,

potentially leaving their previous unit vacant.

- Subsequent Links: Another household moves into the vacated unit,

leaving their own unit vacant, and so on.

- Termination: The chain ends if a unit is not vacated (e.g., a new

household forms), if the unit remains vacant/is demolished, or if the mover

comes from outside the market (e.g., international migration).

|

|

Recent real-world

data from Austen

and

Minneapolis

are frequently used by economists to demonstrate that

massive supply increases can

directly lower rents across an entire market.

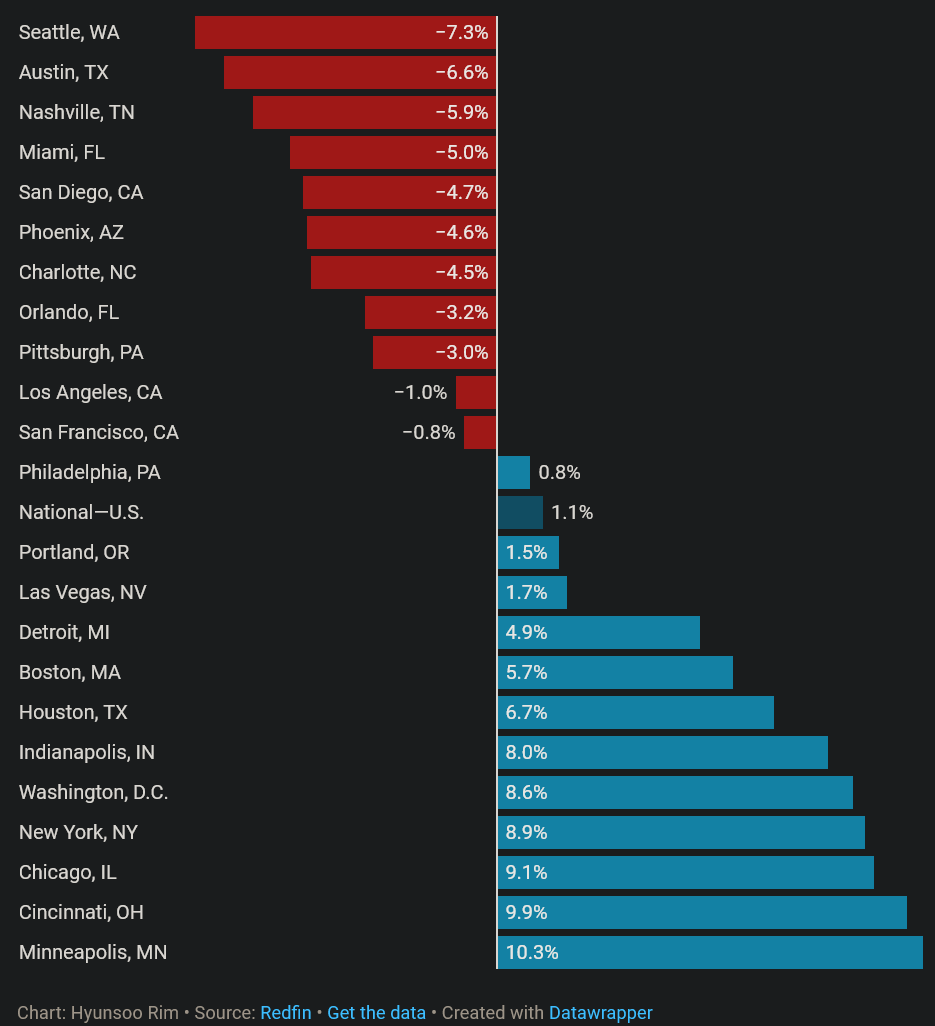

Austin, Texas: The " Supply Surge" Example,

became a national case study in 2023–2024 when it added more apartment

units per capita than any other major U.S. city.

|

Rent Declines: By mid-2024, Austin's median

rent had fallen by 6.6% to 7%

year-over-year. Some data showed declines of up to 17.1% from the 2022 peak for certain unit

types. |

|

The "Escalator" Effect: Research by

Pew Charitable Trusts

found that adding new market-rate housing

actually led to the

steepest rent drops in Class C buildings (older, less expensive

units).

|

Class A (New/Luxury): -2.6%

rent growth. |

|

Class C (Older/Affordable):

-11.4% rent growth. |

|

|

Mechanism: As high-income renters "traded

up" to new luxury buildings, landlords of older buildings were forced to

offer significant concessions

(like 1–2 months free rent) and lower base rents to remain competitive. |

Minneapolis, Minnesota:

Zoning Reform Results

was the first major U.S. city to eliminate single-family-only zoning and scrap parking minimums.

|

Bending the Curve: While rents rose nationally by double digits

post-pandemic,

rents remained

remarkably stable. Between 2017 and 2024,

increased its housing stock by roughly

12%, resulting in rent growth

that was 13% lower than the rest of the state. |

|

Actual vs. Counterfactual: A

2025 study from the Minneapolis Fed estimated that without these supply reforms, rents

would have been

17.5% to 34% higher than they are today. |

|

Affordability Impact: Families

are estimated to save

$1,700 per year in rent compared to what they would have paid if

the city followed statewide trends. |

Annual Change In Rent

by Metro Areas (April 2024)

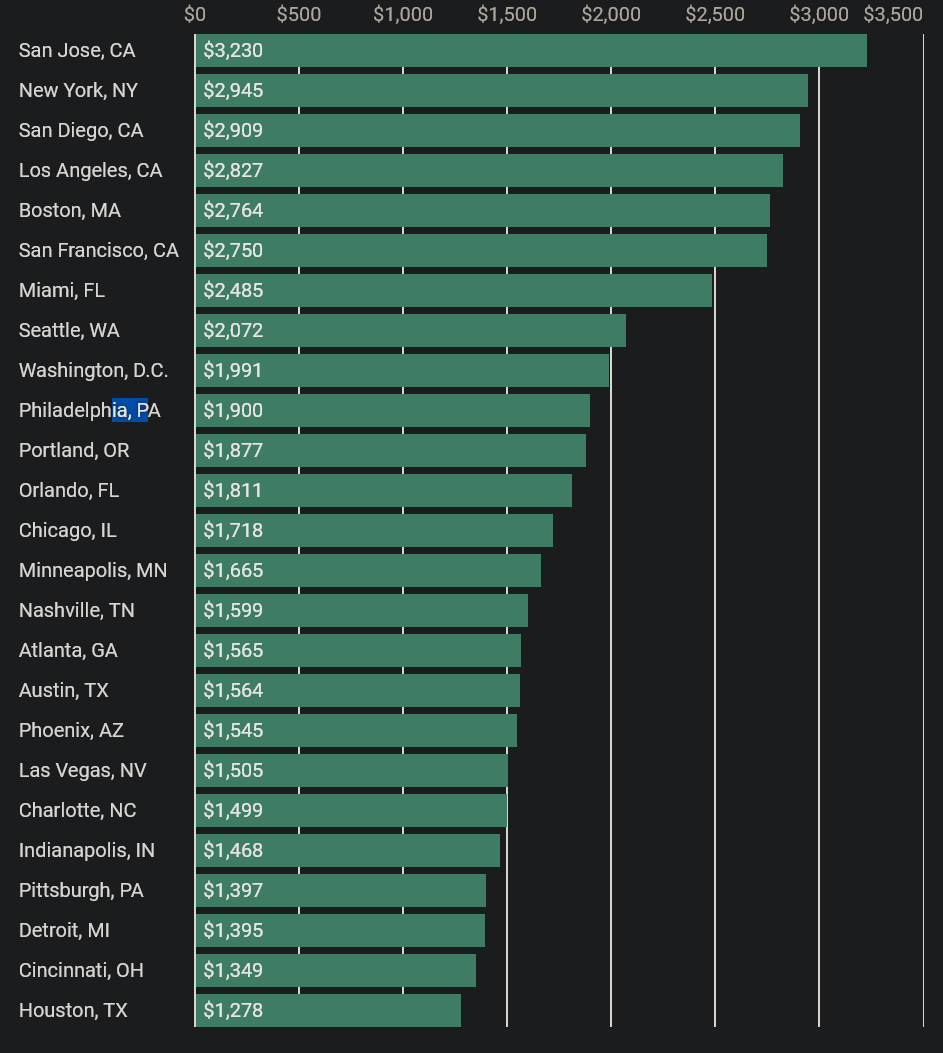

Median Asking Rent By

Metro Areas (April 2024)

|

Theoretical Framework

The research utilizes a "residential diversion ratio" to capture how

households substitute between neighborhoods. Price effects of new supply in

one submarket on another consist of:

| Direct Effects: Proportional to the diversion ratio between the

two specific submarkets. |

| Indirect Effects: Proportional to the product of diversion ratios

across a chain of intermediary submarkets (the vacancy chain). |

--------------------------------------------------------------------------------

3. Methodology and Data Scope

The study utilizes the Census Bureau’s Master Address File (MAF) and

MAF Auxiliary Reference Files (MAF-ARF) to construct residential

histories for the entire U.S. population from 2000 to 2021.

| Sample: 1.5 million new units (single-family suburban and

multifamily urban) built between 2009 and 2018 across the 17 most populous

U.S. metropolitan areas. |

| Housing Types Analyzed:

| Low-Density Suburban Single Family (SSF): Homes in below-median

density tracts outside the principal city. |

| High-Income Urban Multifamily (UMF): Units in 20+ unit

buildings in above-median income tracts within five miles of the Central

Business District. |

|

--------------------------------------------------------------------------------

4. Descriptive Findings: The Lifecycle of Vacancy Chains

Chain Length and Duration

The research establishes that vacancy chains are generally short lived:

| 90% of chains terminate within three rounds of moves. |

| The cumulative number of vacancies levels off by the sixth round. |

| Most effective vacancies are created within a one-year horizon of

the initial move; chains do not grow substantially longer when followed over

a four-year period. |

Submarket Connectivity and Income

The composition of vacancies shifts as chains progress, but the starting

point heavily influences the outcome:

| Metric |

High-Income Urban Multifamily (UMF) |

Low-Density Suburban Single Family (SSF) |

| Total Vacancies per Unit (4-yr) |

~0.9 |

~0.9 |

| Round 1 Vacancies (Top Quintile Income) |

71% |

40% |

| Round 6 Vacancies (Below-Median Income) |

37% |

44% |

| Vacancies in Low-Income Tracts |

0.15 |

0.25 |

| Vacancies in Low-Income/High-Density |

0.03 |

0.015 |

Regional vs. Local Impact

| UMF Impact: Primarily loosens demand in the highest-end segments.

It takes 50 new high-income urban units to generate

just one vacancy in a low-income, very high-density tract. |

| SSF Impact: While SSF creates more vacancies in below-median

income tracts per unit than UMF, its connection to the densest urban centers

is even weaker, requiring 100+ units to generate a single vacancy in a

low-income, high-density neighborhood. |

--------------------------------------------------------------------------------

5. Simulation Exercise: Price and Welfare Effects

The researchers conducted 1,000 simulations to link observed vacancy chains

to unobserved economic outcomes.

| Average Elasticity of Urban Rent Premium: -0.3 (meaning a 10%

increase in supply correlates with a 3% decrease in the urban rent premium). |

| Predictive Value: The number of vacancies created in a

neighborhood is a highly accurate predictor of price and welfare effects.

This is significant because vacancy chains are easier to observe than the

complex cross-price demand parameters usually required for such economic

modeling. |

| Geographic Variation: Welfare and price benefits are not

distributed equally. They are strongly correlated with the geographic

distribution of moves within the vacancy chains. |

--------------------------------------------------------------------------------

6. Conclusion and Policy Implications

The research challenges the "supply-skeptical" view by confirming that new

market-rate housing does create vacancies in lower-income segments

through filtering. However, it also qualifies the "pro-supply" view by showing

that the geographic and categorical incidence of these benefits is

highly localized.

Final Assessment: Continued suburban expansion

is an ineffective tool for addressing urban housing affordability for

low-income households.

Because vacancy chains are short and submarkets are only weakly connected, increasing the supply of housing in one area (the suburbs)

does not meaningfully ripple into the most constrained segments of another

area (the urban core).

To alleviate rising costs in dense urban centers, policy must focus on

increasing density and supply within those specific central neighborhoods.

|